When considering the myriad choices for home financing, homebuyers might wonder, “Are mortgage points worth it?” By paying special fees to the lender, you can sometimes get a lower interest rate. However, the points are no small expense. It’s important to weigh the pros and cons before deciding.

What are points on a mortgage?

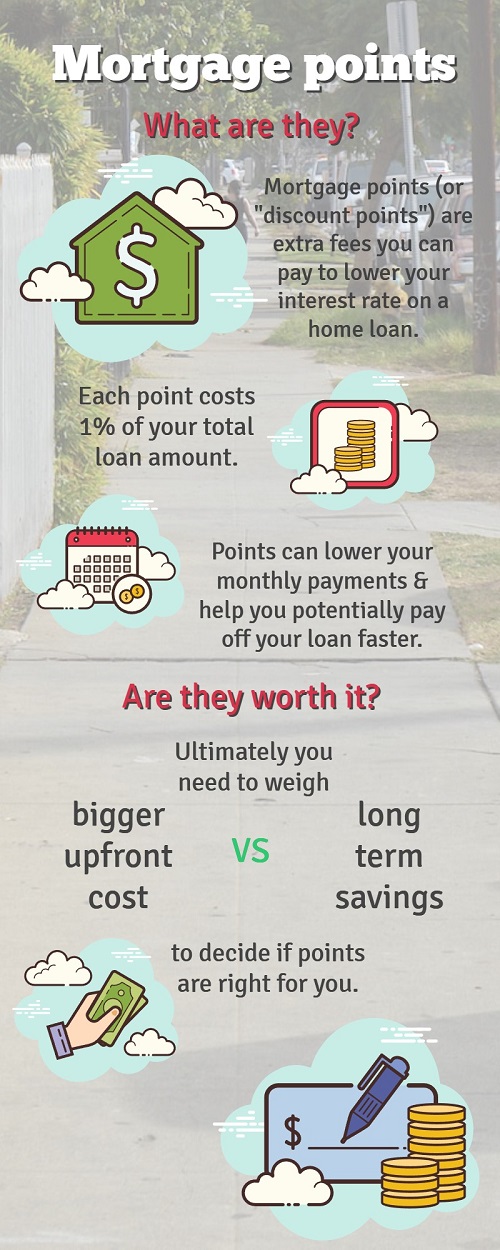

Mortgage points, also called discount points, are fees paid by borrowers to reduce loan interest rates. Terms and conditions of different points vary from one lender to the next, but the pricing is typically standard across lenders. Each individual point costs 1% of your loan amount.

Why buy mortgage points?

Mortgage points have the potential to significantly lower your monthly mortgage payments and help you save money in the long term. As interest rates rise, using points can be a worthwhile strategy for making your mortgage more affordable.

Mortgage point disadvantages

Lower monthly payments and a lower interest rate are excellent advantages of mortgage discount points, but what are the downsides? One major disadvantage is, to truly save money, you must stay in the home for a long enough time to reach a “break even point,” or the amount of time it will take for your savings to be greater than the amount you pay out.

If you have plans to refinance or sell your home in the near future, you may lose money on discount points by not taking full advantage of the prepaid interest.

Is buying mortgage points worth it?

Buying points from your mortgage lender might be worth it in some cases, but every financial situation is different. If you plan to stay in your home for the entirety of the loan term, you’ll eventually benefit from the upfront cost of points and save a large amount of money.

However, homebuying already comes with significant upfront costs, and you may not want to add another to the list. Instead, some financial experts suggest putting extra money toward a larger down payment instead, as this can also affect your interest rate in some cases.

Are mortgage points right for you? Ultimately, only you can decide. Keep these factors in mind when considering your options for home financing.

About the Author

Kimberly Hering

Kimberly Hering's devotion to helping people achieve their real estate goals stems from her genuine enjoyment of the process. Whatever the task, Kimberly makes it her mission to get it done, however she can, without compromising her client's needs. Often, that means thinking outside the box. After working with Kimberly, clients describe her as being Trustworthy, Creative, Patient, Highly Skilled, Attentive to the Process and having a lot of Integrity.

After spending more than 15 successful years working on Wall Street, Kimberly transitioned into Real Estate, joining Alain Pinel Realtors, then moving to Zephyr, now Corcoran Global Living, in 2018. During her career on Wall Street, Kimberly was a Vice President working as an Institutional Equity Salesperson for Montgomery Securities for 10 years. She covered the top money managers throughout the US and Canada. She joined Jefferies & Co as a Senior Vice President managing the Western Region Institutional Sales group, while continuing to cover the top money managers.

Kimberly leverages her extensive experience selling equities to top money managers throughout the US and Canada, to successfully negotiating any Real Estate transaction seamlessly for her clients. Kimberly is well versed in Marin's neighborhoods, towns, cities, and education system.

Living in the Bay Area for 35 years, 25 years in Marin and having 2 sons in local Marin schools, Kimberly spends a lot of time volunteering in the community and serving on various local Boards. Kimberly has a collection of resources ranging from the best local breakfast spots to vetted contractors. With her reliable list of valuable resources, Real Estate experience and unsurpassed knowledge of Marin's many communities, Kimberly can guide her clients through every aspect of a Real Estate transaction seamlessly.

Relocating to Marin, downsizing, upsizing, first time home buying, final home purchase or sale, or a lot to build a dream home, no matter the undertaking, Kimberly works seamlessly until the job at hand is completed with 100% satisfaction.